Cryptocurrency Securities Exemptions: A Guide to Avoiding SEC Registration

Imagine spending months building a groundbreaking blockchain project, only to find out that your token launch is technically an illegal offering of unregistered securities. For many founders, this is the ultimate nightmare. In the eyes of the U.S. government, the line between a "utility token" and a "security" is often thinner than a digital wallet's private key. However, you don't always have to go through the grueling, expensive process of full SEC registration to stay legal. There are specific cryptocurrency securities exemptions that can act as a safe harbor if you know how to use them.

The Foundation: Why Some Tokens Are Securities

Before looking at the exits, you have to understand why you're in the room. The SEC doesn't have a specific "crypto law"; instead, they use a decades-old standard called the Howey test. The Howey test is a legal standard used to determine whether a transaction qualifies as an "investment contract" and therefore a security. Essentially, if there is an investment of money in a common enterprise with a reasonable expectation of profits derived from the efforts of others, the SEC considers it a security.

This is where things get tricky. If you're just selling a tool that people use on your network, you might be fine. But if you're selling a token to fund development with the promise that the token's value will moon because of your hard work, you've likely created a security. While the SEC recently clarified in March 2025 that certain proof-of-work mining activities don't constitute securities, most token-based fundraising still falls under this umbrella.

Federal Registration Exemptions: The Common Pathways

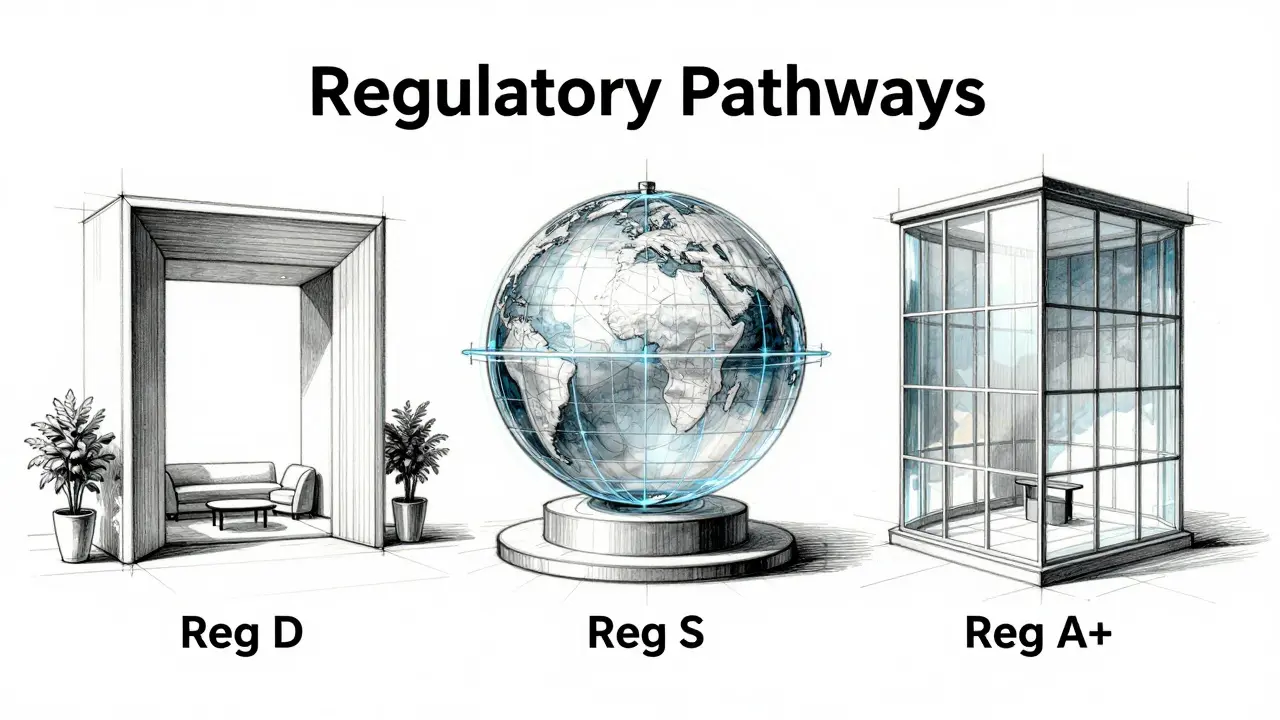

If your token is deemed a security, you aren't necessarily forced into a full public IPO. Most crypto projects leverage specific regulations to bypass the heaviest registration burdens. Depending on who you're selling to and how much you need to raise, one of these three pathways usually fits best:

- Regulation D: This is the go-to for private sales. It allows you to sell tokens to "accredited investors" (people with high net worth or professional experience) without registering the offering. It's the primary way institutional money enters the crypto space.

- Regulation S: If you aren't targeting U.S. citizens, this is your best bet. It exempts offerings made offshore, allowing projects to scale globally while staying outside the immediate reach of the SEC.

- Regulation A+: Think of this as a "mini-IPO." It allows you to raise up to $75 million from the general public. It requires SEC approval and more disclosure than Reg D, but it's much simpler than a full public registration.

| Exemption | Target Audience | Funding Cap | Complexity |

|---|---|---|---|

| Regulation D | Accredited Investors | Unlimited (usually) | Low |

| Regulation S | Non-U.S. Investors | Unlimited | Moderate |

| Regulation A+ | General Public | Up to $75 Million | High |

The New Frontier: Tokenized Securities and NFTs

We are entering a phase where the government is finally trying to catch up with the tech. In May 2025, Commissioner Hester Peirce hinted at a potential exemptive order that would allow firms to use Distributed Ledger Technology (DLT) to issue and settle securities. This would basically create a legal bridge for "tokenized securities," allowing the efficiency of blockchain to meet the safety of regulated markets, provided that fraud and manipulation are kept in check.

There is also a growing movement to exempt NFTs (Non-Fungible Tokens). While some NFTs are clearly just digital art (and thus not securities), others act like shares in a company. By March 2025, indicators suggested that the SEC might officially carve out "art NFTs," allowing creators to raise funds without the heavy burden of securities laws, as long as the NFT doesn't promise a financial return based on the creator's effort.

Navigating State-Level Rules

Federal law is only half the battle. Each U.S. state has its own rules. Take Louisiana, for example. Under the Virtual Currency Business Act, most people engaging in crypto business need a license. However, they provide exemptions for those already regulated by the Securities Exchange Act of 1934 or the Commodities Exchange Act of 1936. They even have a "small-scale" exemption for those whose business activity doesn't exceed $35,000 annually. This means that while the SEC might be okay with your token, your state's financial regulator might still want their cut or a license application on their desk.

Learning from the Failures: Enforcement Precedents

If you're wondering why legal teams are so terrified of the SEC, look at the history books. The 2017 DAO Report was a wake-up call, proving that decentralized autonomous organizations aren't invisible to regulators. Then there was the Telegram case in 2019, where the SEC successfully blocked the Gram token sale, reminding everyone that "global" doesn't mean "exempt." More recently, the 2022 BlockFi settlement-resulting in a $100 million fine-showed that crypto lending products are also in the crosshairs. These cases prove that the SEC prefers to sue first and ask questions later if you launch without a clear exemption strategy.

The Practical Side of Compliance

Getting an exemption isn't as simple as checking a box. It requires a rigorous legal analysis of your token's utility. For instance, if you offer a pooled mining investment where users share profits, you are almost certainly dealing with an investment contract, regardless of whether you use a blockchain. The SEC's April 2025 guidance on crypto asset markets emphasizes that disclosure requirements still apply. Even if you are exempt from registration, you cannot lie to investors or omit material facts about the project.

The current trend is moving toward a "regulatory turning point," where the SEC and CFTC (Commodity Futures Trading Commission) are coordinating more closely. This is good news for the industry; it means registered exchanges might finally have a clear path to list assets that fit into these exemption frameworks without fearing a sudden cease-and-desist letter.

Does a utility token automatically exempt me from securities laws?

No. While a token that is purely used for a service (like a digital ticket) is less likely to be a security, the SEC looks at the overall aeconomy of the token. If you sold the token in a presale to fund the development of that utility, the act of selling it was likely a securities offering, even if the end product is a utility token.

What is the difference between Regulation D and Regulation S?

Regulation D focuses on who the buyer is (accredited investors) within the U.S., while Regulation S focuses on where the transaction happens (outside the U.S.). Many projects use both simultaneously to cover both high-net-worth U.S. investors and the global market.

Can I use NFTs to raise money without SEC registration?

Possibly, but it's risky. If the NFT is sold as a piece of digital art, it generally isn't a security. However, if you tell buyers that the NFT will increase in value because you're going to build a gaming empire, the SEC may classify it as an investment contract.

What happens if I ignore these exemptions and launch anyway?

You risk severe penalties, including massive fines (like BlockFi's $100 million settlement), being forced to offer a full refund to all token holders, and potential criminal charges for the founders.

Are Bitcoin ETPs considered securities for all purposes?

Generally, yes, but there are weird exceptions. For example, the Office of Government Ethics (OGE) considers Bitcoin ETP shares as "Excepted Investment Funds" rather than standard securities for the purpose of federal employees' financial disclosures.

Next Steps for Project Founders

If you're currently planning a token launch, start by mapping out your investor base. If you're only targeting institutional players, a Regulation D framework is your fastest route. If you're aiming for a global community, ensure your marketing doesn't target U.S. residents to keep Regulation S viable. Above all, avoid using words like "investment," "profit," or "return" in your whitepaper, as these are red flags that practically invite the SEC to apply the Howey test to your project.

Caiaphas Konkol

April 20, 2026 AT 11:48The Howey test is essentially a relic used by a dying bureaucracy to maintain a stranglehold on wealth distribution while they figure out how to tax the void. It is painfully obvious that these "exemptions" are just narrow corridors designed to let the elite play in the sandbox while the actual innovators get crushed by the weight of antiquated 1940s legislation.

Robert Mosolygo

April 20, 2026 AT 21:10The coincidence of these "clarifications" appearing exactly when institutional blackrock-style entities are moving in is not lost on anyone with a functioning brain. They aren't helping the industry; they are sculpting the regulatory landscape to ensure that only the pre-approved corporate overlords can survive. The SEC is simply the enforcement arm of a larger systemic consolidation of power. Every one of these Reg D or Reg S pathways is just a way to keep the retail investor-the actual blood of the system-at a distance while the insiders feast. It's a meticulously planned heist masquerading as consumer protection.

Eric Raines

April 22, 2026 AT 10:27Actually, if you'd read the fine print on Reg A+, you'd realize it's practically a trap for anyone who isn't already a millionaire. I've seen a dozen projects try the "mini-IPO" route only to get bled dry by legal fees before they even hit the market. It's basic math, people.

Candace Sherrard

April 22, 2026 AT 18:55It is quite fascinating to observe how we attempt to map the fluid, decentralized nature of blockchain onto these rigid, state-defined legal structures, almost as if we believe a set of rules written for railway bonds can adequately describe the architecture of a global trustless network. There is a certain poetic irony in the way we scramble for "safe harbors" within a system that is fundamentally designed to prevent the very autonomy that cryptocurrency seeks to instantiate in the first place, leading us to wonder if the goal is truly compliance or if we are simply decorating the walls of our own regulatory cage.

Kyle Bush

April 23, 2026 AT 20:23GET THE USA BACK ON TOP!! 🇺🇸 We need to crush these offshore scams and keep the money in our own backyard where it belongs! 🦅💰 If you aren't following US law, you're just a thief in a fancy digital costume! 🚫📉

Jason M

April 25, 2026 AT 07:42Let's look at this as an opportunity to grow! While the legal hurdles are intimidating, the projects that actually take the time to get their compliance right are the ones that will survive the next decade. It's all about building a foundation of trust. If you're scared of the SEC, you're probably doing something wrong anyway! Let's get after it!

Gary Lingrel

April 26, 2026 AT 04:01imagine thinking a "guide" on the internet is enough to save you from a federal lawsuit lol 🙄 just another day of people pretending they can game the system while the house always wins

Yvette P

April 27, 2026 AT 14:54Oh sure, let's just lean on the "utility token" defense and hope the SEC doesn't notice the massive treasury sale during the seed round, because that's totally how the legal machinery works in the real world. I'm sure the Reg S offshore pivot is just *wonderful* for those who enjoy spending their weekends filling out KYC paperwork for jurisdictions that are essentially just a post office in the Caribbean. It's truly a masterclass in regulatory arbitrage where we pretend the 'technology' is the point while we actually just shuffle ledger entries to avoid a cease-and-desist. Absolute peak efficiency right here.

Tara Aman

April 28, 2026 AT 21:24I totally agree that the Reg D route is the safest way for those starting out! It's so great to see a clear path for institutional growth!

Benjamin Forg

April 29, 2026 AT 23:27its all a distraction anyway the sec is just a front for the central banks to kill the competition before they lose control of the fiat printing press

praveen subbiah

May 1, 2026 AT 04:49The ambition to create such a complex system is truly breathtaking! My heart beats for the developers fighting these giants! 🇮🇳

Hannah Rubia

May 3, 2026 AT 03:42I would suggest that founders prioritize a thorough legal audit before selecting an exemption pathway, as the misclassification of a token can lead to catastrophic financial liabilities.

Clair Geary

May 3, 2026 AT 13:08this is such a handy breakdown for anyone trying to navigate the wild west of crypto laws

Matthew Morse

May 4, 2026 AT 22:49too long didnt read basically just dont get caught

Lisa Camp

May 5, 2026 AT 00:32STOP WAITING FOR PERMISSION! Either build the future or get out of the way! If you're too scared of a piece of paper from DC to innovate, you don't deserve the gains!

Sarah Ingrams

May 5, 2026 AT 16:14sounds stressful

Ellie Drews

May 6, 2026 AT 21:31I think it's really helpful to have these different options so people don't feel like they have to choose between being illegal or being bankrupt.

Jagdish Sutar

May 8, 2026 AT 11:17Welcome everyone! It is wonderful to see such a diverse discussion on how different countries can adapt to these digital assets!

Kathleen Bergin

May 9, 2026 AT 21:12Just use Reg S and don't talk to Americans. Simple.

Charlie Queen

May 10, 2026 AT 12:32Love the energy in this thread! 🌟 Everyone just trying to figure out the new world order together! 🌍✨

debashish sahu

May 11, 2026 AT 20:48In many ways, the struggle for legal recognition mirrors the journey of early trade guilds in India, where tradition and new regulation often clashed before finding a balance.