Real-World Distributed Ledger Technology Use Cases in Finance

The financial world is moving away from a world where one central bank or server holds the "truth." For decades, we've relied on centralized databases that act as the ultimate authority, but that's changing. Distributed Ledger Technology is a decentralized system where multiple identical copies of transaction records are maintained across a network of computers, known as nodes. While many people confuse it with just Bitcoin, DLT is the broader engine that allows a network to agree on data without needing a middleman to vouch for it.

We've reached a tipping point. In 2025 and 2026, we are seeing a shift from "cool experiments" to actual production systems. Banks are no longer just running pilots; they are deploying live infrastructure to cut costs and kill off the delays that plague traditional banking. If you've ever wondered why a cross-border wire transfer takes three days to clear, you're looking at the problem DLT is designed to solve.

The Big Shift: From Centralized to Distributed

To understand why this matters, look at how a standard bank works. Every bank has its own private ledger. When you send money to someone at another bank, those two separate ledgers have to "talk" to each other and reconcile. This process is slow, manual, and prone to errors.

DLT flips this script. Instead of separate books, everyone on the network shares a single, synchronized version of the truth. This creates a shared state that is immutable-meaning once a transaction is written, you can't just go back and change it. To make this work without a central boss, the network uses Consensus Mechanisms is the process by which nodes in a distributed network agree on the validity of a transaction.

You'll see two main flavors here:

- Permissionless: Like Bitcoin, where anyone can join and "mine" blocks using Proof-of-Work. It's incredibly secure but consumes massive amounts of energy.

- Permissioned: Preferred by banks. These are invite-only networks that use Proof-of-Stake or other efficient methods, offering the speed and privacy that a regulated company needs.

Cross-Border Payments and the End of the Wait

Sending money across borders has been a nightmare for years. It usually involves a chain of "correspondent banks," each taking a small fee and adding a few hours of delay. Swift is the global provider of secure network connectivity for financial institutions. They've recognized that the old model is broken. In late 2025, Swift integrated a blockchain-based shared ledger into its stack.

This isn't just a cosmetic update. By using a shared ledger, Swift allows banks to move tokenized value in real-time. Instead of sending messages *about* money, they are moving the actual digital asset. This removes the need for tedious reconciliation. For a small business (SME) importing goods from Asia to New Zealand, this means payments that used to take days now happen in seconds, drastically improving cash flow.

Tokenization and Digital Assets

Tokenization is essentially taking a real-world asset-like a building, a gold bar, or a government bond-and turning it into a digital token on a ledger. This allows for Fractional Ownership is the process of dividing a high-value asset into smaller, tradable shares on a digital ledger.

Imagine a commercial property worth $100 million. Normally, only a few ultra-wealthy investors could touch that. With tokenization, that property can be split into a million tokens. Now, a regular investor can own a piece of that building. Because the ledger handles the ownership records and transfers automatically, you don't need a mountain of paperwork to prove who owns what.

Governments are doing this too with Central Bank Digital Currencies (CBDCs) is digital forms of a nation's sovereign currency issued and regulated by its central bank. CBDCs allow central banks to distribute money directly to citizens or facilitate interbank settlements without the friction of legacy systems.

Automating Finance with Smart Contracts

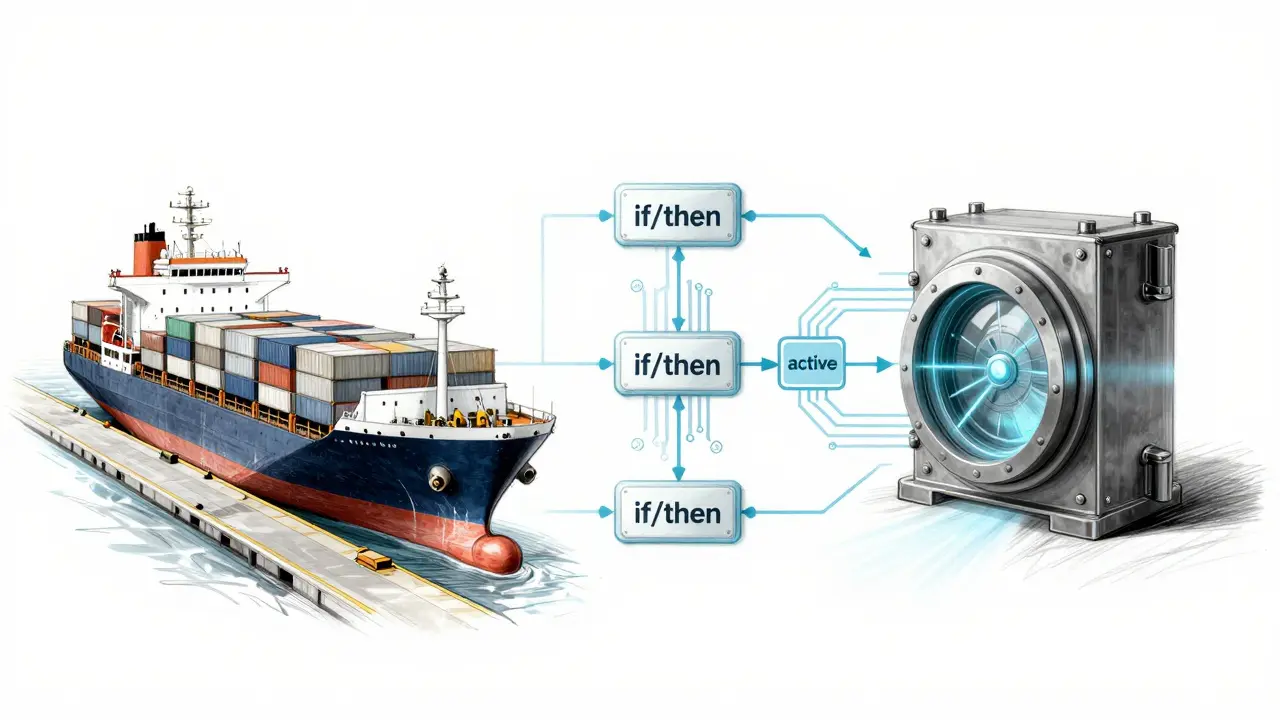

The real magic happens when you add Smart Contracts is self-executing contracts with the terms of the agreement directly written into lines of code. Think of these as "if/then" statements for money. "If the ship reaches the port of Auckland, then release the payment to the supplier."

In traditional finance, this requires an escrow agent or a bank to verify the event and move the money. A smart contract does it automatically. This eliminates counterparty risk-the fear that the other person won't pay up after the work is done.

| Feature | R3 Corda | Hyperledger Fabric |

|---|---|---|

| Primary Focus | Regulated Banking & Insurance | General Enterprise & Supply Chain |

| Privacy Model | Need-to-know basis (point-to-point) | Channel-based isolation |

| Architecture | Permissioned / Specialized | Modular / Permissioned |

| Common Use Case | Syndicated Lending / CBDCs | KYC / AML Compliance |

Solving the Oracle Problem: Real-World Data

One major hurdle for DLT has been the "Oracle Problem." A blockchain is great at knowing what happened *inside* the chain, but it's blind to the outside world. It doesn't know if a plane landed or if the price of gold dropped. An "oracle" is the bridge that feeds external data into the smart contract.

If the oracle provides wrong data, the smart contract executes the wrong action. This is why many projects stayed in the pilot phase. However, we're seeing breakthroughs. For example, DZ BANK collaborated with Google Cloud to create Smart Derivative Contracts (SDCs). They built a secure pipeline to feed market data into their ledger, ensuring the data's integrity before it ever touches the contract. This is a critical step in moving complex financial derivatives-which are worth trillions-onto a distributed ledger.

Trade Finance and KYC Efficiency

Trade finance is still shockingly reliant on paper. Letters of Credit, Bills of Lading-all these are often mailed or faxed across the globe. DLT turns these documents into digital assets. When a buyer and seller agree on terms, the ledger tracks the movement of goods and the release of funds simultaneously.

Then there's KYC (Know Your Customer). Currently, every bank you open an account with puts you through the same tedious identity check. With a distributed ledger, a user's identity can be verified once and then "shared" (via a secure cryptographic pointer) with other institutions. You don't send your passport copy ten times; you give ten institutions permission to see your verified status on the ledger.

The Road Ahead: Integration and Hurdles

We aren't in a perfect world yet. Transitioning from a controlled test environment to a live production system introduces new risks. Attack vectors that don't exist in centralized systems-like 51% attacks or smart contract bugs-can lead to massive losses if not handled properly.

Moreover, the complexity of setting up these systems is high. You can't just "install" a blockchain; you need to coordinate with other banks, regulators, and tech providers to agree on the standards. But the pressure is on. Institutions that stay stuck in the pilot phase will find themselves unable to compete with the speed and efficiency of those who have fully embraced the decentralized shift.

Is Distributed Ledger Technology the same as Blockchain?

Not exactly. Blockchain is a *type* of DLT. All blockchains are distributed ledgers, but not all distributed ledgers use a chain of blocks. For example, some DLTs use different data structures (like Directed Acyclic Graphs) to achieve the same goal of decentralized record-keeping.

How do smart contracts reduce risk in finance?

They remove the need for a trusted third party to oversee a transaction. Because the contract automatically executes when specific conditions are met, there's no risk of one party refusing to pay or a middleman delaying the process. This eliminates the "counterparty risk."

What is the "Oracle Problem"?

Blockchains are closed systems. They can't "see" outside data (like a stock price or weather report) on their own. An oracle is a third-party service that feeds this data into the blockchain. The "problem" is that if the oracle is compromised or wrong, the smart contract will execute based on false information.

Can DLT really replace traditional banking?

It's less about replacing banks and more about replacing the *plumbing* they use. Banks will still provide the interface and regulatory compliance, but the way they move money and assets behind the scenes will shift from slow, centralized databases to fast, distributed ledgers.

Why do banks prefer permissioned networks over public ones?

Privacy and control. On a public blockchain (like Ethereum), every transaction is visible to everyone. Banks need to keep client data confidential and must be able to reverse transactions in case of legal disputes-things that are very difficult on a truly permissionless, public chain.

Next Steps for Implementation

If you're a financial professional or a developer looking to enter this space, the first step is moving beyond the hype. Start by identifying a specific friction point-like a slow settlement process or a repetitive KYC check-rather than trying to "blockchain everything." Focus on interoperability; the future isn't one single blockchain, but a web of different ledgers (Corda, Fabric, etc.) talking to each other through layers like Swift's new infrastructure.

Prachi Bhadarge

April 15, 2026 AT 14:09Oh sure, because banks are just *known* for being cutting edge and not clinging to COBOL systems from the 70s until the very last second. 🙄

Shannon Kelly Smith

April 15, 2026 AT 15:42Exactly! The shift to tokenization is where the real magic happens for retail investors. 🚀 It's all about democratization of assets! Let's get everyone in on this! 🌟📈

Shantal Sanjur

April 16, 2026 AT 18:24Please. "Permissioned" is just a fancy word for "we still control everything and can delete your money whenever we want." It's not decentralized if a board of directors can just vote to change the ledger. The whole point of DLT was to get rid of the suits, but now the suits are just building their own private clubs with the same old rules wrapped in new jargon. It's a total scam to make us think things are changing while the central banks just figure out how to track every single cent we spend in real-time with those CBDCs. Absolute surveillance nightmare waiting to happen. 🙄

Kevin Lư

April 17, 2026 AT 23:56Honestly sounds pretty cool, though I'm probably too lazy to actually read the whitepapers. Just give me the app that makes my money move faster, lol.

Chintu Parikh

April 18, 2026 AT 06:54I must express my profound agreement with the assertions regarding cross-border payment efficiency. The integration of a shared ledger within the Swift framework represents a monumental leap forward in financial synchronization. It is truly inspiring to witness the global community collaborating to dismantle systemic frictions that have hindered international trade for decades. Such innovation will undoubtedly catalyze economic growth for small to medium enterprises across the globe. I am genuinely energized by the prospect of a more fluid and interconnected financial ecosystem! 🤝

Gillian Kent

April 20, 2026 AT 05:13I thnk its great that we are lookng at differnt ways to move money. its about time we stop relyng on stuff that takes days to clear. lawdy, we live in the future but banking feels like the stone age sumtimes.

Ian Chait

April 21, 2026 AT 20:17Told ya it's all about the CBDC trap. The 'Oracle Problem' is a joke-they'll just feed the ledger whatever lies the state wants. Pure centralisation disguised as 'distributed' garbage. Proper bloody shambles if you ask me, and the luddites in the City are just playing along for the grants. 🇬🇧

Trudy Morse

April 22, 2026 AT 01:54DLT is essentially the ontological shift of trust from institutions to mathematics. Simple as that.

Adam Mann

April 24, 2026 AT 00:58It is so wonderful to see these technologies becoming accessible. I remember when the idea of a shared ledger seemed like something out of a sci-fi novel, but now we are talking about actual real-world applications that could help a small business owner in a remote village get paid instantly. It's a beautiful thing when technology serves humanity in a way that bridges the gap between different cultures and economies, and I believe that if we keep focusing on inclusivity, the financial world will become a much friendlier place for everyone regardless of where they start from.

Alex Long

April 25, 2026 AT 14:16Mid.

Sean Douglas

April 25, 2026 AT 18:15The sheer, unadulterated agony of waiting three days for a wire transfer is a tragedy that has scarred my very soul! To think that we've endured this bureaucratic purgatory for so long while the solution was staring us in the face is simply exquisite in its cruelty. My heart bleeds for the SMEs caught in the crossfire of legacy systems! 🎭

Andrew Southgate

April 27, 2026 AT 01:37The point about the Oracle Problem is really the crux of the whole thing. If you're building a smart contract for a derivative, the data integrity is everything. I'd recommend anyone looking into this to study the Chainlink model or how Google Cloud is handling those secure pipelines because a single point of failure in the data feed completely negates the security of the ledger. It's a complex hurdle, but once solved, the scalability for things like automated insurance payouts or trade finance is virtually limitless. Keep pushing the boundaries, folks!

Gaurav Undirwade

April 28, 2026 AT 15:07It is highly regrettable that many of you fail to recognize the moral imperative of maintaining a structured regulatory framework. Without a central authority to ensure ethical conduct, these distributed systems risk becoming havens for the unscrupulous. One must maintain the highest standards of integrity when implementing such disruptive technology, lest we descend into a state of financial anarchy where the powerful prey upon the uninformed.

Vicky Duffala

April 29, 2026 AT 02:38The concept of fractional ownership is just wild. Like, I could technically own 0.0001% of a skyscraper in New York while sitting in my pajamas? That's the kind of energy I'm here for. 🏢✨ It's a total paradigm shift in how we view value and possession.

Mike Kempenich

April 29, 2026 AT 06:07I'm cautiously optimistic about this. I think the biggest hurdle isn't the tech, but the people who benefit from the current slow system. But hey, the momentum is there, and it's hard to stop a train once it's left the station. We're moving in the right direction.