Future of Cryptocurrency Taxation: What You Need to Know in 2026

Cryptocurrency isn't just a investment anymore-it's a financial activity that now lives under the microscope of tax authorities. If you bought, sold, traded, staked, or even received crypto as a gift in 2025, you’re already part of a new tax reality. The rules changed dramatically last year, and they’re only getting tighter. Forget the old days of vague reporting. In 2026, the IRS and exchanges are working together like never before, and ignorance is no longer an excuse.

Every Crypto Transaction Is Taxable

You don’t need to sell crypto to owe taxes. Even swapping one coin for another counts. Buying Bitcoin with Ethereum? Taxable event. Using Dogecoin to pay for a coffee? Taxable event. Receiving staking rewards or airdrops? That’s income. The IRS still treats crypto as property, not currency, which means every movement triggers a potential tax liability. There’s no such thing as a free lunch in crypto anymore.When you earn crypto through mining, staking, or a job, it’s taxed as ordinary income. The value at the moment you receive it becomes your cost basis. If you later sell that crypto for more than what you received, you owe capital gains. If you sell for less, you can claim a loss-but only if you follow the new rules.

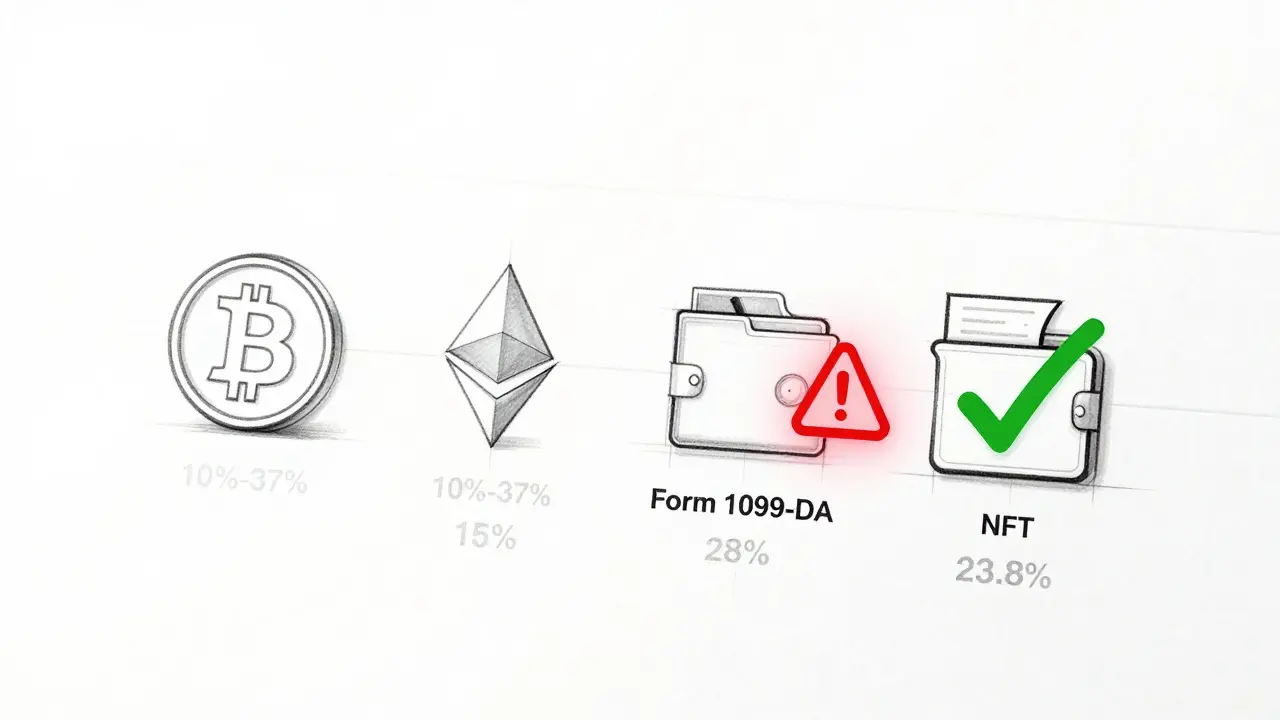

2025’s Biggest Change: Form 1099-DA

Starting January 1, 2025, every U.S. crypto exchange and platform had to start issuing Form 1099-DA. Think of it as the crypto version of Form 1099-B, which brokers use for stocks. This form reports all your sales, trades, and disposals. Exchanges now track your entire transaction history-when you bought, when you sold, and what you traded it for. That data gets sent directly to the IRS.This doesn’t mean you’re off the hook. You still need to report everything, even if your exchange doesn’t. Why? Because not all crypto activity happens on exchanges. If you moved coins between wallets, used a decentralized exchange, or received crypto from a peer-to-peer transaction, those aren’t captured by Form 1099-DA. You’re still responsible for tracking those.

Wallet-by-Wallet Accounting Is Now Required

The IRS killed the old “universal cost basis” method. You can no longer average your purchase prices across all your wallets. Now, you must track cost basis wallet by wallet. If you bought Bitcoin on Coinbase, then moved it to Ledger, then sold it from Ledger-you need to know exactly what you paid for that specific batch of Bitcoin when it was originally acquired. This applies to every single wallet you use, whether it’s a hardware device, a mobile app, or a DeFi protocol.This change hits hard. Many people held crypto across multiple platforms for years without keeping detailed records. Now, they’re scrambling to reconstruct transaction histories from screenshots, emails, and blockchain explorers. If you can’t prove your cost basis, the IRS assumes it’s $0. That means your entire sale amount becomes taxable gain.

Long-Term vs. Short-Term: The One-Year Rule Still Matters

Holding crypto for more than a year still gives you a massive tax break. Short-term gains (held less than a year) are taxed at your regular income rate-up to 37%. Long-term gains (held over a year) are taxed at 0%, 15%, or 20%, depending on your income.In 2025, the brackets shifted slightly. For single filers, the 15% long-term rate now starts at $48,350 and goes up to $533,400. Above that, you pay 20%. Add the 3.8% Net Investment Income Tax if your income exceeds $200,000 (single) or $250,000 (married), and your top rate jumps to 23.8%. That’s higher than most stock investors pay.

And here’s a curveball: NFTs and certain collectible digital assets are taxed at 28% on long-term gains. That’s the same rate as art or vintage cars. If you bought an NFT for $5,000 and sold it two years later for $20,000, you’d owe 28% on the $15,000 profit-not 15%.

Wash Sales Are Coming for Crypto

President Biden’s 2025 budget proposal isn’t law yet-but it’s likely to pass. The IRS wants to apply the wash sale rule to cryptocurrency. Right now, if you sell Bitcoin at a loss and buy it back the next day, you can claim that loss on your taxes. That’s called tax-loss harvesting, and it’s a popular strategy.Under the new rule, if you sell crypto at a loss and repurchase the same or “substantially identical” asset within 30 days, you can’t claim the loss. The loss gets deferred until you sell again without repurchasing. This is already standard for stocks. Crypto is next. If you’re using automated trading bots or frequent swaps, this could wipe out your tax savings.

Charitable Donations Still Work-Better Than Ever

One of the few remaining loopholes? Donating crypto directly to a charity. If you give Bitcoin, Ethereum, or any other digital asset you’ve held over a year, you can deduct the full fair market value on the date of donation. And you don’t pay capital gains tax on the appreciation.For example: You bought 1 ETH for $2,000. It’s now worth $4,500. You donate it to a nonprofit. You claim a $4,500 deduction. You owe $0 in capital gains. That’s a win-win. Many charities now accept crypto directly through platforms like The Giving Block or BitGive. Just make sure you get a receipt and document the transaction.

What Happens If You Don’t Report?

The IRS has been quietly building a crypto enforcement unit. In 2025, they matched over 1.2 million crypto transaction reports from exchanges with tax returns. If your Form 1099-DA says you sold $15,000 worth of crypto and you didn’t report it? You’ll get a letter. Then a notice. Then an audit. Penalties can hit 25% of the unpaid tax, plus interest that compounds monthly. And if they think you’re hiding income intentionally? That’s fraud-and criminal.Even if you’re not caught this year, the IRS now has access to blockchain analytics tools. They can trace wallet addresses across platforms. They can identify patterns. They can link your identity to your on-chain activity. It’s not science fiction-it’s happening right now.

How to Stay Compliant in 2026

You can’t wing it anymore. Here’s what you need to do:- Use a crypto tax software like Koinly, CoinTracker, or TokenTax to import all your wallet addresses and exchange histories.

- Export and back up every transaction from every platform you’ve ever used-even ones you’ve closed.

- Track self-transfers between wallets. If you moved 0.5 BTC from Wallet A to Wallet B, record the cost basis at the time of transfer.

- Don’t assume your exchange did everything. Check Form 1099-DA carefully. It may miss off-exchange activity.

- If you’re unsure, hire a CPA who specializes in crypto. Most general tax pros still don’t understand wallet-by-wallet accounting.

What’s Next?

The future of crypto taxation isn’t about banning crypto-it’s about integrating it into the existing financial system. Expect more reporting requirements, tighter links between DeFi platforms and tax authorities, and possibly even real-time transaction tagging. Some countries are already testing blockchain-based tax reporting systems. The U.S. is following.Don’t wait for a notice. Get your records in order now. The next tax season won’t be forgiving. The rules are clear. The tools are here. The IRS is watching. Your job isn’t to avoid taxes-it’s to pay them correctly.

Do I have to pay taxes on crypto I received as a gift?

Yes. Receiving crypto as a gift doesn’t trigger tax when you get it. But when you later sell or trade it, you owe capital gains tax based on the original donor’s cost basis. If you don’t know the donor’s basis, the IRS may treat it as $0. Always get documentation from the sender.

What if I lost access to an old wallet? Can I still file taxes?

You still need to report any crypto you sold or traded-even if you can’t access the wallet anymore. If you can’t prove the cost basis, the IRS assumes it’s $0. That means the full sale amount is taxable. Try recovering the wallet using seed phrases or backups. If you can’t, keep records of when you last accessed it and any transaction history you can find. You may need to explain the loss to the IRS.

Are decentralized exchanges (DEXs) exempt from reporting?

No. While DEXs like Uniswap or PancakeSwap don’t issue Form 1099-DA, your transactions on them are still taxable. You’re responsible for tracking every swap, trade, or liquidity provision. Many crypto tax tools now support DEX integrations via wallet addresses. You must report these manually.

Can I use FIFO, LIFO, or specific identification for crypto?

Specific identification is now the only allowed method. You must identify the exact units of crypto you’re selling and their original cost basis. FIFO (first-in, first-out) and LIFO (last-in, first-out) are no longer permitted under IRS guidance as of 2025. You must track each batch of crypto separately.

What happens if I mine crypto but never sell it?

You still owe income tax on the fair market value of the mined crypto at the time you received it. Even if you never sell, you must report it as income on your tax return. The value becomes your cost basis. If you sell later, you’ll pay capital gains on any increase since receipt.

Prakash Patel

March 19, 2026 AT 21:33Yeah right, like the IRS actually knows what a wallet address is. They're still figuring out how to spell 'blockchain'. I've been holding since 2017 and never filed a single crypto tax. Still here. Still rich. They'll catch up... maybe in 2035.

Elizabeth Kurtz

March 21, 2026 AT 20:46As someone who’s filed crypto taxes for 5 years straight, I get how overwhelming this feels. But honestly? The tools exist now. Koinly linked to my MetaMask, Ledger, and 3 DEXs in 10 minutes. I cried when I saw my capital gains were lower than I thought. You don’t have to be a tax genius-you just have to be consistent. And yes, gifts matter. Always ask for the basis. It’s not rude, it’s responsible.

john peter

March 23, 2026 AT 09:28The IRS’s new regime is not merely bureaucratic-it is epistemologically inevitable. The ontological framework of decentralized finance has been subsumed under the state’s sovereign apparatus of capital accumulation. To resist this is to deny the dialectical progression of monetary history. The blockchain is not a tool of liberation-it is the very mechanism through which capital is refined, quantified, and taxed. You are not owning crypto. Crypto is owning you. And now, it is reporting you.

Marc Morgan

March 23, 2026 AT 11:16So the government now tracks every time I buy Dogecoin to pay for my burrito. Cool. Next they’ll be auditing my TikTok likes. At least I can still use crypto to buy weed in states where it’s legal… oh wait. Never mind. The feds still hate that too. 🤡

Kira Dreamland

March 24, 2026 AT 16:11Just wanted to say thank you for this breakdown. I was terrified of filing this year. I used CoinTracker, imported all my wallets, and it actually showed I had a net loss. I’m going to file with a CPA who gets crypto. It’s worth every penny. You’re not alone in this.

shreya gupta

March 25, 2026 AT 11:55Interesting how Americans treat crypto like a tax loophole. In India, we don’t even have a 1099-DA. We just pay 30% flat on every transaction. No deductions. No exceptions. You think this is bad? Wait until your country adopts our system. Then you’ll learn what real compliance looks like. And no, you can’t write it off as 'investment'. It’s gambling. With taxes.

Derek Lynch

March 25, 2026 AT 13:18You’re all overthinking this. Stop panicking. Use software. Track your buys. Know your basis. File. Done. This isn’t rocket science-it’s spreadsheet math. If you’re still confused, hire someone. $300 is cheaper than an audit. And if you’re sitting on gains? Donate some to charity. It’s literally the only legal way to keep your cake and eat it too. Do it. Now. Before they change the rule again.

Dionne van Diepenbeek

March 26, 2026 AT 02:51Wash sales coming for crypto? Yeah right. Like the government cares enough to enforce it. I sold my ETH at a loss bought it back 2 hours later. They don’t even know I exist. Let them try to trace my 17 wallets. I’ve got more addresses than my cat has naps.

Graham Smith

March 27, 2026 AT 05:02The integration of blockchain-based tax reporting systems into the global financial architecture represents a paradigmatic shift in fiscal sovereignty. The current regulatory framework, predicated on centralized intermediaries, is functionally obsolete. One must now engage in granular on-chain metadata analysis to ensure compliance with the emergent regulatory ontology. Failure to implement wallet-by-wallet accounting constitutes a breach of fiduciary epistemology. I recommend consulting a Certified Crypto Tax Specialist (CCTS) immediately.

Katrina Smith

March 28, 2026 AT 08:06form 1099-da? more like form 1099-dont-ask-me-again. i lost my seed phrase in 2021. now i gotta pay taxes on 10 btc i can’t even access. the irs is just gonna take it from my next paycheck. whatever. i’m still gonna buy more when the price drops. again. forever.

Lauren J. Walter

March 28, 2026 AT 13:41I didn’t even know I had to report my staking rewards until my cousin told me she got audited. Now I’m paralyzed. I’ve got 37 transactions from 2023 I can’t find. I’m not sleeping. I keep checking my email for IRS letters. I think I’m going to move to Portugal. Or maybe just disappear.

Carol Lueneburg

March 30, 2026 AT 05:45YOU GOT THIS 💪💖 I DID IT TOO! I used TokenTax + linked my hardware wallet + even added my DeFi positions. It was scary at first but now I feel so proud. I even donated 0.2 ETH to a kids’ STEM charity and got a $900 deduction. I’m crying happy tears. You’re not alone. I believe in you! 🌈✨

Brenda White

March 31, 2026 AT 00:16why do people think the irs cares about crypto? they dont even know what a nft is. i sold my ape for 50k last year and never said a word. theyre too busy chasing people who didnt file for unemployment. theyre gonna miss this whole thing. until they dont. then its too late. just wait.

Tobias Wriedt

March 31, 2026 AT 11:54God sees your crypto transactions. Every swap. Every trade. Every airdrop. You think you’re anonymous? You’re not. The blockchain is a digital confession booth. And the IRS? They’re just the earthly messengers. Repent. File. Donate. Or face the consequences. 🙏🔥

Ernestine La Baronne Orange

April 2, 2026 AT 00:22Do you have any idea how many hours I’ve spent reconstructing transaction histories from 2019? I had to dig through 12 years of email archives, 37 screenshots, 5 broken hard drives, and a single PDF from a now-defunct exchange. I cried. I screamed. I almost quit crypto forever. And now? I have to track every single wallet. Every. Single. One. And if I make one mistake? They’ll come for my house. My car. My dog. My cat. I don’t even have a cat. But they’ll take it anyway. This isn’t taxation. This is psychological warfare.

Manali Sovani

April 2, 2026 AT 12:20This article is a joke. In India, we pay 30% tax on all crypto gains. No deductions. No exceptions. No software. No forms. Just pay. And yet, people still trade. Why? Because they are fools. You think America is harsh? Wait until your government starts freezing wallets. Then you will understand real control.

Konakuze Christopher

April 4, 2026 AT 11:09They’re coming for your keys. This is phase one. Next: mandatory wallet registration. Then: real-time transaction surveillance. Then: crypto bans. Don’t believe me? Look at China. Look at Russia. They’re already building blockchain surveillance networks. This isn’t tax policy. It’s prelude.

S F

April 5, 2026 AT 16:24Let me be clear: America is being hijacked by tech elites who think they’re above the law. Crypto was supposed to be freedom. Now it’s just another IRS trap. You think they care about you? They care about your money. And they’re not stopping until every Satoshi is accounted for. This is socialism with a blockchain.

Angelica Stovall

April 6, 2026 AT 06:49Everyone here is acting like this is new. It’s not. The government has been tracking crypto since 2014. They just didn’t have the tools. Now they do. And they’re not asking. They’re taking. If you’re still using unregulated wallets, you’re not a pioneer-you’re a target. And you’re going down with everyone else.

Taylor Holloman.

April 7, 2026 AT 08:36I’ve been reading this whole thread and I just want to say… you’re all doing better than you think. It’s scary, yeah. But you’re here. You’re trying. You’re not ignoring it. That’s huge. I used to be terrified too. Now I’ve got a spreadsheet with color-coded wallets and a little sticky note that says ‘You got this.’ And honestly? I’m proud of myself. You will be too.

Bryan Roth

April 8, 2026 AT 12:46Look-I’ve helped 12 people file crypto taxes this year. Some were total beginners. One guy had 37 wallets from 8 different exchanges. We used Koinly, imported everything, and found he actually had a $12k loss. He cried. We celebrated. The point isn’t to fear the IRS. It’s to outsmart the system before it outsmarts you. Use the tools. Ask for help. Don’t suffer in silence. You’re not alone. And you’re not behind. You’re just getting started.